From PC Pioneers to AI Architects: Taiwan's Tech Odyssey

From PC Pioneers to AI Architects: Taiwan's Tech Odyssey

In the heart of Asia, a small island nation has scripted one of the most remarkable tales in modern industry. This is the story of Taiwan's technology sector, as seen through the eyes of Huang Ching-yung, president of the Electronic Times, who has witnessed its evolution over four decades. From humble beginnings in DIY computer assembly to dominating the global AI supply chain, Taiwan's journey is a blend of ingenuity, luck, and relentless adaptation. Let's trace this path, step by step, with visuals that capture the essence of each era.

The Dawn of the PC Era: 1980s - Building from Scratch

It all began in 1985, a pivotal year for Taiwan's tech scene. Back then, the industry was synonymous with Chung-Hua Mall, where clever entrepreneurs assembled "white-box" PCs—knockoffs of Apple II and early IBM compatibles. Visionaries like Kwo-Ting Li, a key government advisor, saw potential in semiconductors and computing. He rallied young talents, including Huang himself, to train under U.S. experts. With government backing, including a $200 million investment in training 20 researchers, Taiwan shifted from illegal copies to legitimate IBM-compatible machines.

This era was marked by disassembly and innovation: motherboards, keyboards, power supplies, and cases were produced separately, fostering companies like Acer, Mitac, and Elitegroup. Intel's 386 CPU and Microsoft's Windows provided the standards, turning Taiwan into a PC powerhouse. Growth was explosive—50-80% annually from 1985 to 1989. But it wasn't easy; prices were cutthroat, embodying the "Price Below Cost" mantra to win U.S. orders.

)

The Boom and Bust: 1990s - Scaling Up and Facing Challenges

The 1990s brought highs and lows. From 1989 to 1992, growth slowed to 10-15% as DOS-based PCs proved clunky. Then, in June 1992, Compaq slashed prices by 40%, narrowing the gap between branded and Taiwanese products. Ironically, this forced U.S. firms to outsource to Taiwan, sparking a tenfold surge from 1992 to 1996. Monthly motherboard production jumped from 40,000 to 400,000 units.

Notebook PCs emerged, with the Industrial Technology Research Institute (ITRI) providing blueprints. Fifty to sixty Taiwanese firms competed fiercely, outpacing Japanese and Korean rivals through cost-cutting prowess. Companies like Hon Hai (Foxconn), Quanta, and Compal rose, fueled by listings on the stock market—Taiwan's first electronic IPO was Lite-On in 1975. The Asian Financial Crisis of 1997-98 barely dented Taiwan, thanks to PC demand.

By the late '90s, scale demanded more: labor shortages pushed manufacturing to China, starting in Guangdong and moving to Kunshan. This "westward march" built ecosystems but sowed seeds for future rivalries.

The Smartphone Shift and Red Supply Chain: 2000s - Globalization and Competition

The 2000s saw Taiwan's PC lines relocate entirely to China by 2000, with the last notebook assembly in Shanghai's Songjiang. This era birthed the "red supply chain" as China nurtured its own ecosystem, leveraging a massive domestic market—peaking at 33% of global smartphone sales.

Apple's iPhone in 2007 revolutionized the industry, benefiting Apple, Samsung, and Chinese suppliers. Taiwan faced pressure: acquisitions attempts by firms like Tsinghua Unigroup targeted TSMC and MediaTek. Beijing's 2008 Olympics boosted China's confidence, leading to U.S.-China tensions. Yet, Taiwan adapted, with firms like Delta Electronics and Quanta thriving in power supplies and servers.

Geopolitical Winds and Return Home: 2010s - Rising Pressures

The 2010s were Taiwan's "dim decade" from 2008-2018, overshadowed by China's golden years. U.S. restrictions post-2018, amplified by COVID-19, urged Taiwanese firms to "return home" for sensitive production. This coincided with smart manufacturing: automation reduced Quanta's workforce from 150,000 in 2018 to 59,000 in 2023, while profits soared from $501 million to $1.28 billion.

TSMC, founded in 1987, became the linchpin with its pure-play foundry model. Heroes like Morris Chang, Charles Kao, and Hu Ting-hua built an ecosystem of over 1,000 companies, concentrated in Hsinchu to Taipei. Population density—Taiwan's "blessing"—enabled tight-knit clusters, unlike Korea's vertical integration.

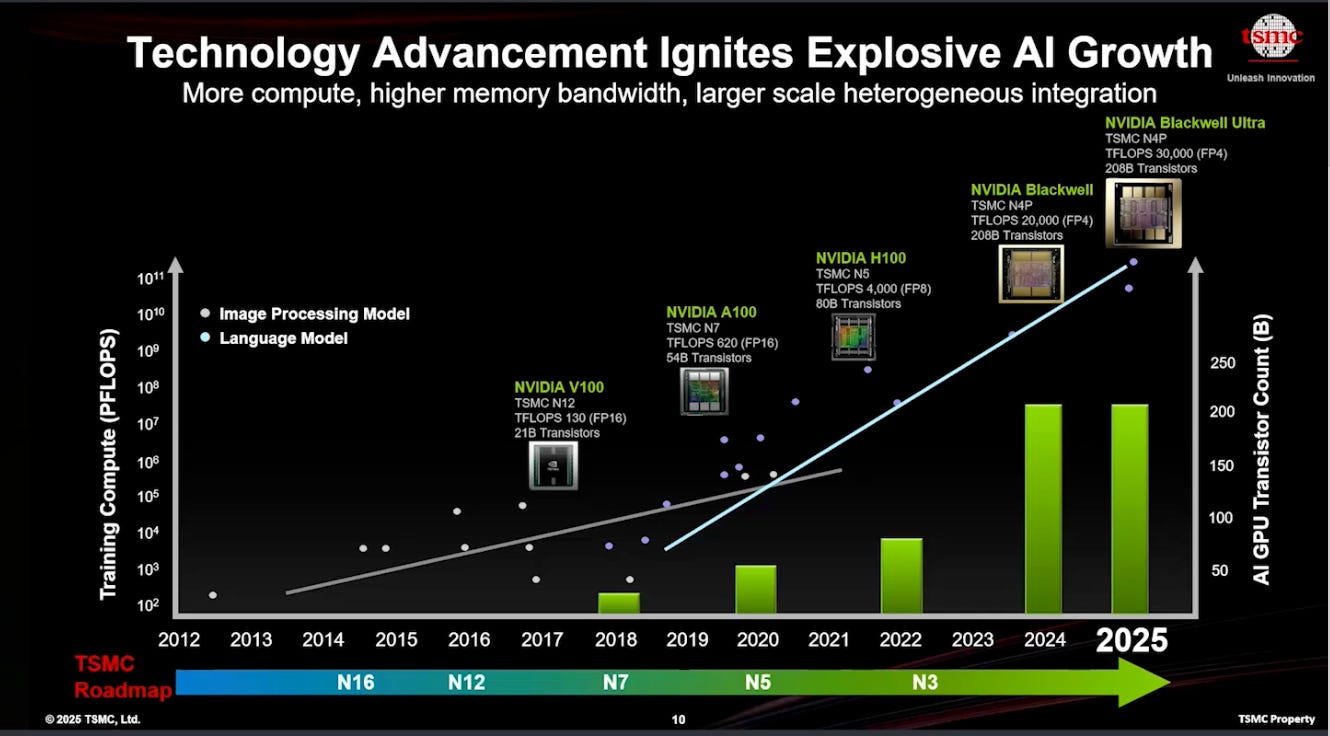

The AI Revolution: 2020s - Taiwan's Golden Age

ChatGPT's 2022 debut ignited AI demand. NVIDIA's revenue exploded from $7.19 billion in Q4 2022 to $65 billion projected for the current quarter—an 8-9x leap. Taiwan captured this: firms like Quanta, Wistron, Hon Hai, and Delta handle servers, with Delta holding over 50% market share in power supplies.

U.S.-China conflicts funneled orders to Taiwan, boosting 2025 revenue to $1.15 trillion across 1,051 listed firms. TSMC's expansions, including in Arizona and Japan, underscore global reach, but Taiwan remains the fastest for fab construction. Jensen Huang, NVIDIA's founder since 1993, credits Taiwan's ecosystem for seamless integration.

Yet, challenges loom: talent shortages (needing 51,000 IC designers by 2031 amid low birth rates) and wealth concentration (1% capturing 99% of gains). Taiwan's strategy? Partner with medium powers like Vietnam, Philippines, and Europe, leveraging density for efficient clusters.

Looking Ahead: A Blessing in Density and Collaboration

Taiwan's story isn't just survival—it's leadership. From PC price wars to AI dominance, it's about ecosystems, not isolation. Population density fosters collaboration; geopolitics demands diversification. As Huang says, hardware can't be easily replaced, and Taiwan's 40-year foundation positions it for another 20-30 years of growth. The future? AI-integrated industries, global partnerships, and sharing prosperity to bridge inequalities.

In this odyssey, Taiwan proves small islands can cast giant shadows in the tech world.

留言

張貼留言